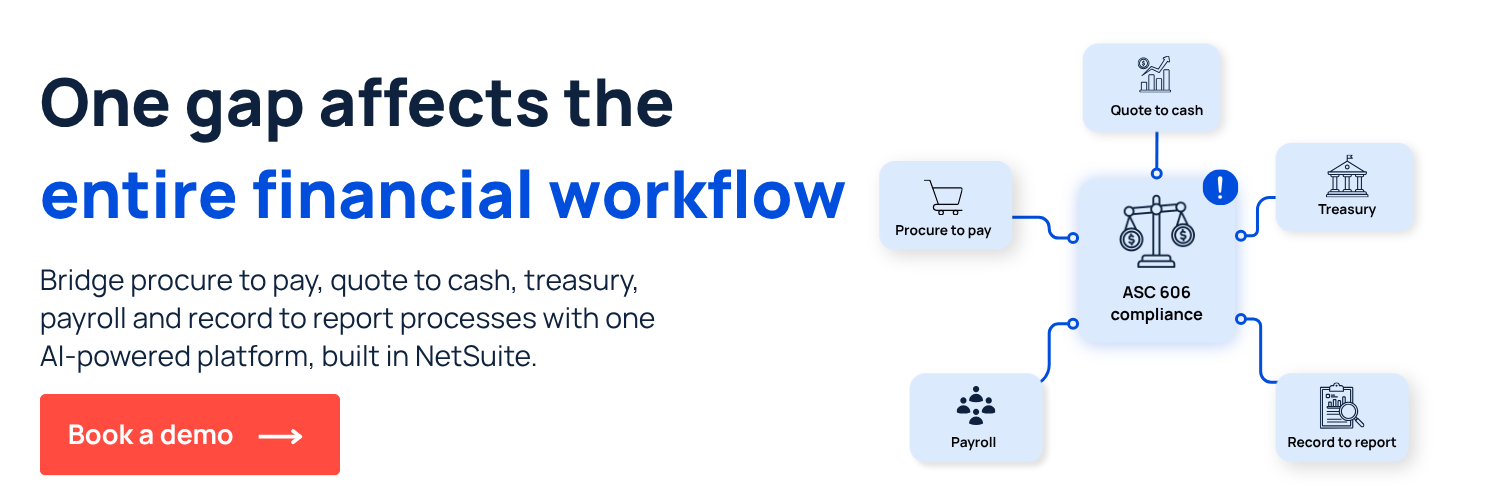

What is ASC 606?

Take the ZoneBilling product tour →Accounting Standards Codification (ASC) 606 is the revenue recognition standard issued by the Financial Accounting Standards Board (FASB) that governs when and how companies recognize revenue from contracts with customers – replacing a collection of industry-specific standards with a single five-step framework applicable across all sectors.

For finance teams – especially those in SaaS, subscription billing and professional services – ASC 606 has significant implications for how billing data is structured, when revenue is posted and how contract modifications are handled in the enterprise resource planning (ERP) system. It took effect for public companies in 2017 and private companies in 2018 and 2019.

Why ASC 606 matters for finance teams

A SaaS company closes a $120,000 contract in March that includes software access for 12 months, a one-time implementation and three months of premium support. Finance now has to figure out how to split the transaction price across three distinct performance obligations, set up a revenue schedule for the software access component, determine when implementation revenue is earned and decide how to handle the support period – and update all of it when the customer upgrades mid-contract.

Compliance with ASC 606 requires billing data and revenue recognition to stay in sync. When a contract is modified – a customer upgrades a plan, adds a seat or cancels early – the revenue schedule must update to reflect the change in the same period. When billing runs outside the ERP, those updates require manual reconciliation between the billing system and the revenue ledger.

That’s the operational reality ASC 606 creates. The standard matters because it requires contracts to be analyzed at the obligation level, not the invoice level – and that analysis must happen correctly every time, at scale.

The ASC 606 five-step model

The five-step model is the framework ASC 606 requires finance teams to apply to every customer contract before revenue can be recognized.

- Identify the contract with a customer: A contract exists when both parties have approved it, each party’s rights are identifiable, payment terms are set, the contract has commercial substance and collection is probable.

- Identify the performance obligations: Performance obligations are the distinct goods or services the company has promised to deliver. For a SaaS company, software access, implementation services and ongoing support may each be a separate performance obligation with its own recognition timing.

- Determine the transaction price: The transaction price includes fixed fees, variable components (usage charges, bonuses, penalties) and any consideration payable to the customer. Variable components must be estimated and may be constrained until it becomes probable that including them won’t result in a significant revenue reversal.

- Allocate the transaction price: When a contract includes multiple performance obligations, the transaction price is allocated to each based on its standalone selling price (SSP). This allocation determines how much revenue is associated with each deliverable and when it can be recognized.

- Recognize revenue when obligations are satisfied: Revenue is recognized when – or as – a performance obligation is satisfied. SaaS subscriptions are typically recognized ratably over the subscription term. Point-in-time deliverables are recognized when control transfers to the customer.

Common ASC 606 compliance challenges for finance teams

ASC 606 compliance breaks down in predictable places. Most finance teams understand the five-step model in theory. The problems show up in the operational layer, where billing systems, contract terms and ERP configuration either support the standard or create manual work around it.

Performance obligation identification at scale

Identifying performance obligations is straightforward on a single contract. At volume, the same analysis has to run consistently across every new contract, every amendment and every renewal. When that identification depends on a revenue accountant reviewing each contract manually, inconsistencies accumulate over time and create disclosure risk. Finance teams that operationalize this step configure their ERP to capture obligation-level data at the point of sale, so recognition schedules generate from structured contract data rather than judgment calls.

Contract modifications that require manual recalculation

When a customer upgrades a plan, adds a seat or cancels early, the original recognition schedule changes. Under ASC 606, that modification may require a cumulative catch-up adjustment, a prospective change or a full reallocation depending on whether the modification adds a distinct performance obligation. When billing runs outside the ERP, those updates require manual reconciliation between the billing system and the revenue ledger, often after the period has already closed.

Standalone selling price (SSP) allocation consistency

SSP allocation requires a defined methodology applied consistently across every contract of the same type. When that methodology lives in a spreadsheet, allocation consistency depends on the person running the model. Changes in product pricing, bundling or discount structure require the model to be updated manually. Finance teams that configure SSP allocation inside the ERP apply the same logic automatically, regardless of who processes the contract.

Variable consideration estimation

Usage-based charges, volume discounts, bonuses and penalties all create variable consideration that must be estimated and constrained before it can be recognized. The constraint condition requires a probability assessment that can be updated as more information becomes available. When variable components are tracked outside the ERP, updating estimates at each reporting period requires a separate reconciliation step that slows close and creates version control risk.

ASC 606 disclosure preparation

ASC 606 requires disaggregated revenue disclosures, contract balance rollforwards and remaining performance obligation summaries. When recognition data lives in spreadsheets rather than the ERP, those disclosures are assembled manually from multiple sources. Finance teams spend close time reconstructing data that should already exist in a reportable format. Disclosure preparation becomes a month-end task instead of a system output.

How teams improve ASC 606 compliance

Operationalizing ASC 606 means building a process where recognition schedules update automatically when contracts change. Here’s how finance teams do it:

- Map contracts to performance obligations at the point of sale: Configure the ERP to identify distinct obligations from contract terms automatically, rather than relying on revenue accountants to interpret each contract manually.

- Configure SSP allocation methodology consistently: Define the standalone selling price methodology – adjusted market assessment, expected cost plus margin or residual – once in the system and apply it consistently to every contract of that type.

- Generate recognition schedules automatically at contract creation: When a contract is entered in the ERP, recognition schedules should generate automatically without manual journal entry setup.

- Handle contract modifications in the same period they occur: When a customer upgrades, cancels or modifies their contract, the recognition schedule should update automatically in the current period without requiring manual recalculation.

- Connect billing events directly to recognition: Link billing triggers to revenue schedule updates so that usage-based charges, renewals and amendments flow through to recognition automatically.

- Generate ASC 606 disclosure reports from the same data: Disaggregated revenue, contract balances and remaining performance obligation disclosures should generate from the same recognition data that drives journal entries – not from separate manual workbooks.

How ZoneBilling supports ASC 606 compliance

ASC 606 compliance holds up when the system handling recognition stays connected to the contracts, billing events and ERP records that drive it. ZoneBilling enhances NetSuite ARM with the automation and flexibility finance teams need to stay compliant at scale, without leaving the native environment.

Key capabilities include:

- Automated performance obligation management. ZoneBilling automatically identifies and manages performance obligations from contracts, subscriptions and billing events, keeping every obligation traceable and in sync with contract terms.

- Automated contract modifications. When a customer upgrades, renews, downgrades or cancels, ZoneBilling automatically adjusts revenue elements and allocations within ARM in the same period the change occurs.

- Compliant revenue automation. ZoneBilling delivers structured data directly to NetSuite ARM for fully compliant recognition under ASC 606 and IFRS 15, so finance teams can focus on review rather than manual reconciliations.

Book a demo today to discover how Zone & Co supports ASC 606 compliance and automate your finance workflow.

.avif)

.png)